Home purchasing is stressful and frequently expensive, except for one Nevada homebuyer who received the deal of a lifetime. Her purchase included many properties when she signed up for a single-family home.

The house she was considering in Sparks, Nevada, was worth $594,481. Yet, according to records from the Washoe County (Nevada) Assessor and Recorder’s Office, she purchased not just her Sparks property but also 84 additional house lots and two additional properties in Toll Brothers’ Stonebrook development off of Reno.

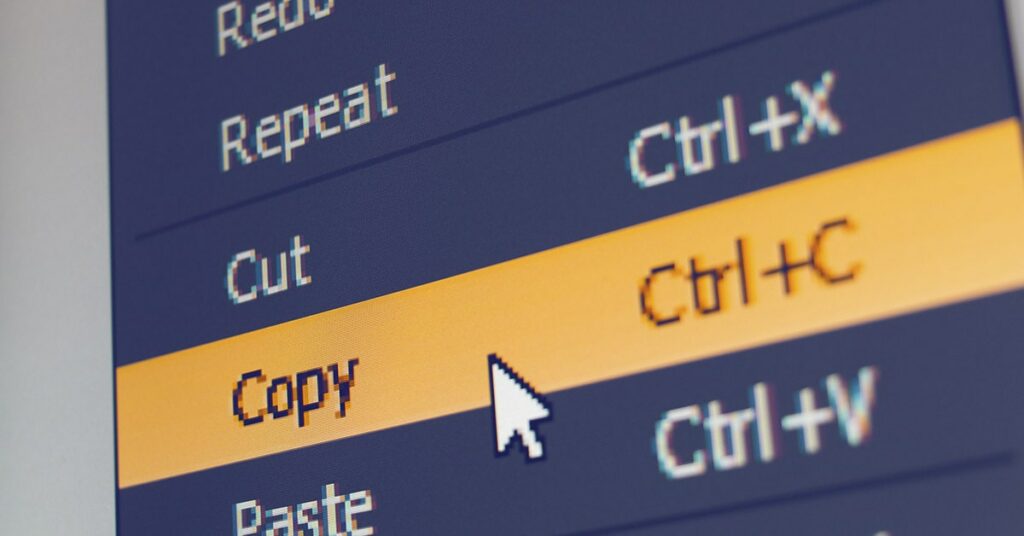

While this may appear a good deal, others had already purchased and developed it on some sites. The assessor’s office reported the transaction and quickly notified Toll Brothers of the problem. How did this mistake happen? All it needed was a simple copy-paste to send millions of dollars in lots to an unwary customer.

“It appears Westminster Title out of Las Vegas copied and pasted a legal description from another Toll Brothers sale when preparing (the homebuyer’s) deed for recordation,” said Cori Burke, Washoe County’s chief deputy assessor.

“Since it was evident that a mistake had been made, our assessment services section immediately contacted Westminster Title to begin repairing the chain of title for the 86 properties transferred in error.”

After transactions like this one, the Washoe County Assessor’s Office updates ownership information. Yet, this update is based on the legal description rather than the parcel number.

This means that according to the formal definition of the transaction, which was officially recorded on July 25, it covers “lots 1 through 85… and Common Areas A and B.”

According to Burke, flagging errors from improper legal descriptions occur “quite frequently,” often due to other copy-paste problems. “This specific instance is just a little more interesting because of the number of lots involved.”

To correct this, the homebuyer must return the title to Toll Brothers. Using the standard process, Toll Brothers can transfer ownership to any new homebuyers.

They wanted to speed up the process because other people had already purchased some of the lots. Nevertheless, that was contingent on the cooperation of the Nevada homebuyer, who now owns 87 residences.

“I believe someone might try to make things tough,” Burke speculated. “But, the title firm also has the purchase offer and acceptance on file, so the intent is very evident.” I believe that would be a loser in court and doubt it frequently occurs, if at all.”

Yet, the corporation did not need to be concerned about the homebuyer’s participation. “True and legitimate ownership was returned on August 9, 2022, through a new document recorded by Westminster Title,” Burke said on August 12. “The Assessor’s Office has updated all connected parcels’ ownership.”

“It’s a fairly terrible time to be a first-time homebuyer right now,” said Moody’s Analytics Chief Economist Mark Zandi. “When high mortgage rates combine with high property prices, affordability is crushed.” As a result, first-time homebuyers are being priced out of the market. Straight-up buyers are locked in since they would have to sell their low-interest-rate property and acquire a higher-interest-rate one. That is quite difficult.”

The typical listing price for single-family homes in the United States in June was $450,000, up 16.9% from June 2021 and more than 31% from June 2020. According to the Mortgage Bankers Association, as a result, mortgage applications had declined to their lowest level in 22 years (MBA).

While some real estate professionals advise customers to wait before purchasing, there is no guarantee that the market will recover. While some people prefer to stay, others rush to buy if the economy worsens.

But Rachel Luna, the owner of Patriot Title in Houston, encourages buyers not to make hasty judgments because they may lose money if they need to sell their new houses.

“Patience,” Luna advised. “When buying a home, your money and long-term economic security matter.” Is it true that you are debt-free? Do you have a three-to-six-month emergency fund set aside?

Will your monthly mortgage payment be 25% or less of your monthly take-home pay? It doesn’t matter if the market is in your favor if you don’t comfortably meet these standards.”